Search Suggestions

- Gold Loan

- Money Transfer

- Mutual Funds

CRIF vs. CIBIL: 10 Must-Know Differences

When it comes to securing a personal loan in India, your credit score plays a crucial role. Two of the most prominent credit bureaus in the country are CRIF High Mark and CIBIL. While both these organizations provide credit scores and reports that lenders use to assess your creditworthiness, there are notable differences between them that borrowers should understand.

Table of Content

Whether you're aiming for a personal loan without CIBIL and income proof, or exploring options for a No CIBIL score loan, knowing the distinctions between CRIF and CIBIL can guide your financial decisions effectively.

What is the CIBIL Score?

CIBIL, short for Credit Information Bureau (India) Limited, is India's leading and widely utilized credit information agency. It evaluates credit scores and reports based on an individual's credit history, compiling data from various credit institutions such as banks and NBFCs. This includes details about credit history, repayment patterns, and outstanding loan amounts. Such information is then utilized to create credit reports and scores, aiding lenders in assessing borrowers' creditworthiness and making well-informed lending decisions.

Get Your Free CIBIL Score Online

What is the CRIF Score?

CRIF full form is the Centre for Research in International Finance, a major credit bureau in India. It keeps track of credit activities, such as loans and credit card transactions, for both individuals and companies. Lenders rely on this information when making decisions about loan approvals. In addition to its credit tracking function, CRIF specializes in providing risk management solutions, including software and consulting services, to help lenders manage the risks associated with lending.

Furthermore, CRIF offers comprehensive support for data collection, analysis, and decision-making to help determine credit scores effectively.

By understanding the key differences, you can better navigate your personal loan application and improve your chances of approval:

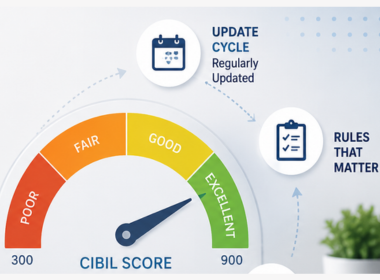

Acceptable Score Range

The CRIF Highmark score ranges from 300 to 900, with 700 being an excellent score. On the other hand, the CIBIL credit score falls between 300 and 900, with a score of 750 being considered good for obtaining credit from potential lenders.

Report Structure

The structure of the credit reports from CRIF and CIBIL varies. A CRIF credit report might present information differently than a CIBIL report. Lenders who use these reports interpret them based on their format, which can influence their lending decisions. Both organisations offer one free credit report per year to individuals.

Data Sources

Both CRIF and CIBIL collect data from various sources, including banks, financial institutions, and non-banking financial companies (NBFCs). However, the comprehensiveness and timeliness of data updates can differ between the two, potentially impacting your credit score.

Report Format

Consumers can access their credit reports from both CRIF and CIBIL online. However, the user interface, ease of access, and the process to obtain these reports might differ. CRIF often provides detailed insights and additional tools to understand your credit health better.

Score Factors

CIBIL Scores take into account payment history, credit utilization, credit mix, and recent credit behaviour. CRIF credit scores are affected by factors such as a person's repayment history, credit utilization, and the length of their credit history.

Market Presence

CIBIL is one of the oldest credit bureaus in India and has a broader market presence compared to CRIF. Many lenders still prefer CIBIL scores due to their long-standing reputation. However, CRIF is rapidly gaining acceptance among lenders.

Licensing

CIBIL is under the official supervision of the RBI and is owned by TransUnion, which is a private unlisted company. On the other hand, CRIF is directly regulated by the RBI.

Weightage

The CIBIL score gives greater importance to recent credit activity and credit inquiries in its calculation. On the other hand, the CRIF Highmark score is calculated by assigning more significance to the length of credit history and the type of credit.

Presence

CRIF High Mark operates worldwide, with a presence in more than 40 countries. On the other hand, CIBIL primarily serves the credit requirements of over 1.4 billion individuals in India.

Impact on Loan Terms

The differences in your CRIF and CIBIL scores can impact the terms of your personal loan, such as interest rates and loan amounts. Lenders might offer more favourable terms based on a higher score from either bureau.

Get Your Free CIBIL Score Online

Understanding the differences between CRIF and CIBIL is crucial for anyone looking to manage their credit profile effectively. Whether you're applying for a personal loan, exploring a No CIBIL score loan, or simply monitoring your credit health. At Muthoot Finance, we have financial experts to cater to your personal loan needs according to your CRIF score vs CIBIL score. Visit your nearest Muthoot Finance branch to know more

- Apply PAN Card Online

- Application

- Eligibility

- Documents Required Forms

- Form 49A

- Form 49AA

- Fees

- Correction & Update

- NRI PAN Card

- Tracking

- Penalty

CATEGORIES

OUR SERVICES

-

Credit Score

-

Gold Loan

-

Personal Loan

-

Cibil Score

-

Vehicle Loan

-

Small Business Loan

-

Money Transfer

-

Insurance

-

Mutual Funds

-

SME Loan

-

Corporate Loan

-

NCD

-

PAN Card

-

NPS

-

Custom Offers

-

Digital & Cashless

-

Milligram Rewards

-

Bank Mapping

-

Housing Finance

-

#Big Business Loan

-

#Gold Loan Mela

-

#Kholiye Khushiyon Ki Tijori

-

#Gold Loan At Home

-

#Sunherisoch

RECENT POSTS

डिफॉल्ट के बाद अपना CIBIL स्कोर कैसे सुधारें: 7 बेहतरीन तरीके

Know More

सोने में निवेश कैसे करें: अपनी संपत्ति को सुरक्षित रखने के स्मार्ट तरीके

Know More

गोल्ड लोन नीलामी की प्रक्रिया क्या है?

Know More

गोल्ड लोन EMI में डिफॉल्ट हो गया है? अभी ये 5 काम करें!

Know More

कम CIBIL स्कोर पर इंस्टेंट पर्सनल लोन: अप्रूवल कैसे प्राप्त करें

Know More

एमसीएलआर बनाम ईबीएलआर - होम लोन पर कौन अधिक बचत करता है?

Know More

इंस्टेंट पर्सनल लोन के लिए ऑनलाइन आवेदन कैसे करें?

Know More

DPD in CIBIL रिपोर्ट : इसका मतलब, कारण और इसे कैसे सुधारें

Know More

1 भोरी सोना क्या है: इसका वजन, कीमत और गोल्ड लोन में भूमिका समझें

Know More

CIBIL स्कोर नियम और अपडेट चक्र: हर उधारकर्ता को क्या जानना चाहिए

Know MoreFIN SHORTS

Can I renew or extend my gold loan after the tenure ends?

Know More

Can I get a loan against 18-karat or 14-karat gold jewelry?

Know More

Will Gold Become the Best Investment by 2030?

Know More

How to Check Loan Details Using Aadhaar & PAN Card?

Know More

How to Calculate Gold Loan Interest Easily?

Know More

Non-Hallmarked Gold in 2026: Is It Safe to Buy?

Know More

Is gold a safe investment during a market crash?

Know More

What is the difference between the 22K and 24K gold price today?

Know More

How often does the gold price change in a day?

Know More

What affects gold prices in India daily?

Know More

Is gold a good investment at current prices?

Know More

Should I buy gold today or wait for a price drop?

Know MoreRelated Posts

{kind=link}

- South +91 99469 01212

- North 1800 313 1212